Open Stock Alert

| Loading... |

A stock market model designed to excel in identifying entry points during trend reversals.

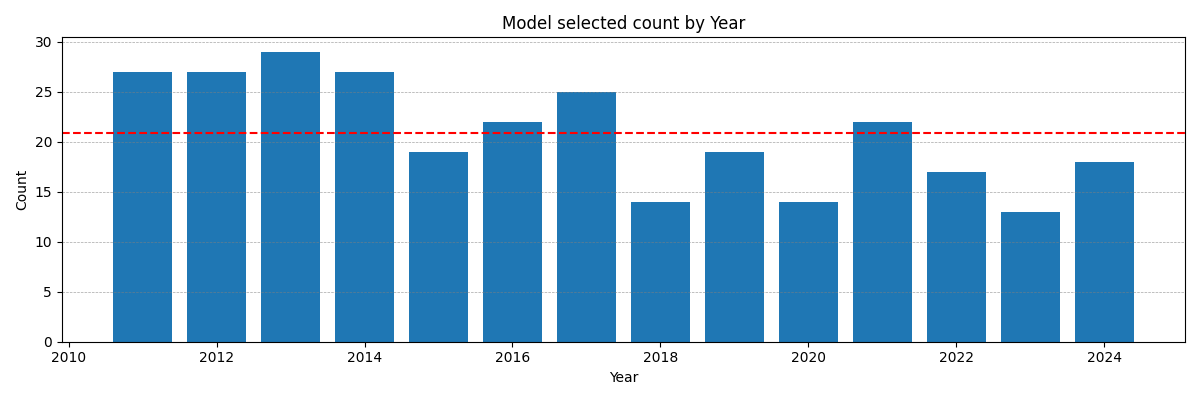

Total Sample Size: 3447 ( started from 2011-01-12 )Model Selected Count: 228 (out of 3,447 trading days, the model selected 160 specific days).

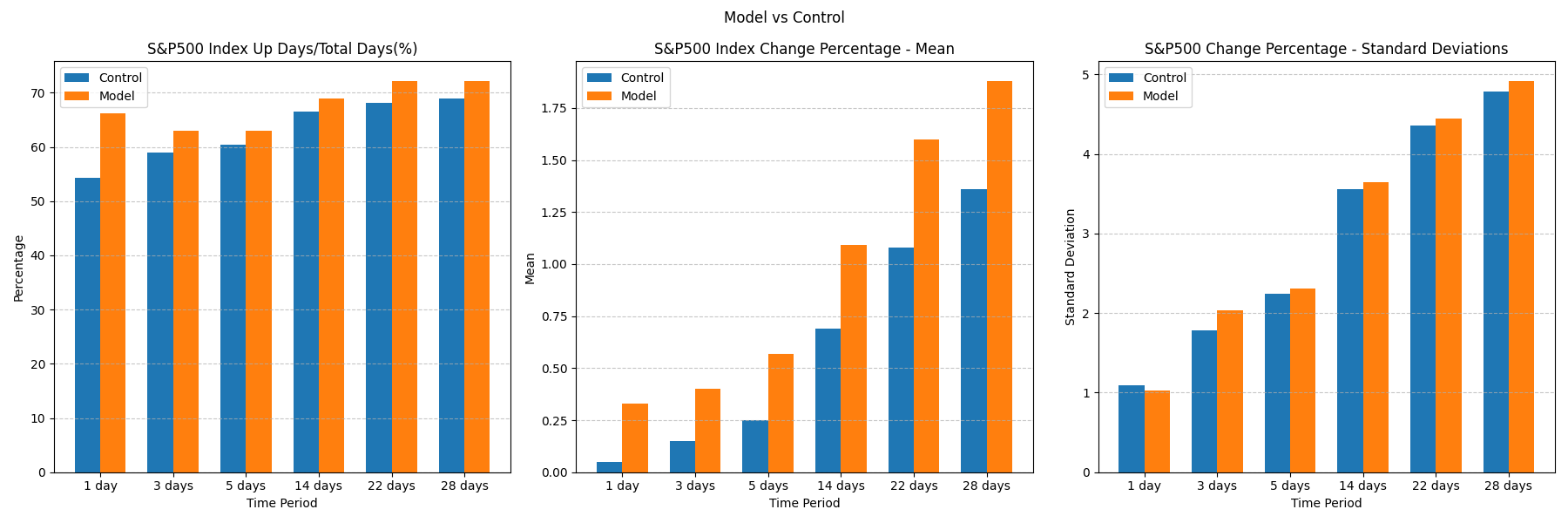

Model Selected Percentage: 6.60% The market performance ( sp500 ) is evaluated at intervals of 1, 3, 5, 14, 22, and 28 trading days following the model's selected dates. The model's performance is assessed based on the 160 selected days, while the control group's performance is measured using all available samples. The datasets sp500_down2, sp500_down3, sp500_down4, and sp500_down5 represent scenarios where the S&P 500 index experienced continuous declines for 2, 3, 4, and 5 consecutive days, respectively.

| Dataframe | Sample Count | Selected Count | Sample Pct | Count of 1day_up | % of 1day_up | % Mean of Chg_1day | StdDev of Chg_1day | Count of 3day_up | % of 3day_up | % Mean of Chg_3day | StdDev of Chg_3day | Count of 5day_up | % of 5day_up | % Mean of Chg_5day | StdDev of Chg_5day | Count of 14day_up | % of 14day_up | % Mean of Chg_14day | StdDev of Chg_14day | Count of 22day_up | % of 22day_up | % Mean of Chg_22day | StdDev of Chg_22day | Count of 28day_up | % of 28day_up | % Mean of Chg_28day | StdDev of Chg_28day |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Control | 3447 | 3447 | 100.00% | 1872 | 54.31% | 0.05 | 1.09 | 2031 | 58.92% | 0.15 | 1.78 | 2080 | 60.34% | 0.25 | 2.24 | 2295 | 66.58% | 0.69 | 3.56 | 2348 | 68.12% | 1.08 | 4.36 | 2375 | 68.90% | 1.36 | 4.79 |

| The Model | 3447 | 228 | 6.60% | 157 | 68.86% | 0.43 | 1.13 | 145 | 63.60% | 0.52 | 2.26 | 151 | 66.23% | 0.8 | 2.45 | 165 | 72.37% | 1.46 | 3.81 | 176 | 77.19% | 2.17 | 4.5 | 176 | 77.19% | 2.47 | 5.03 |

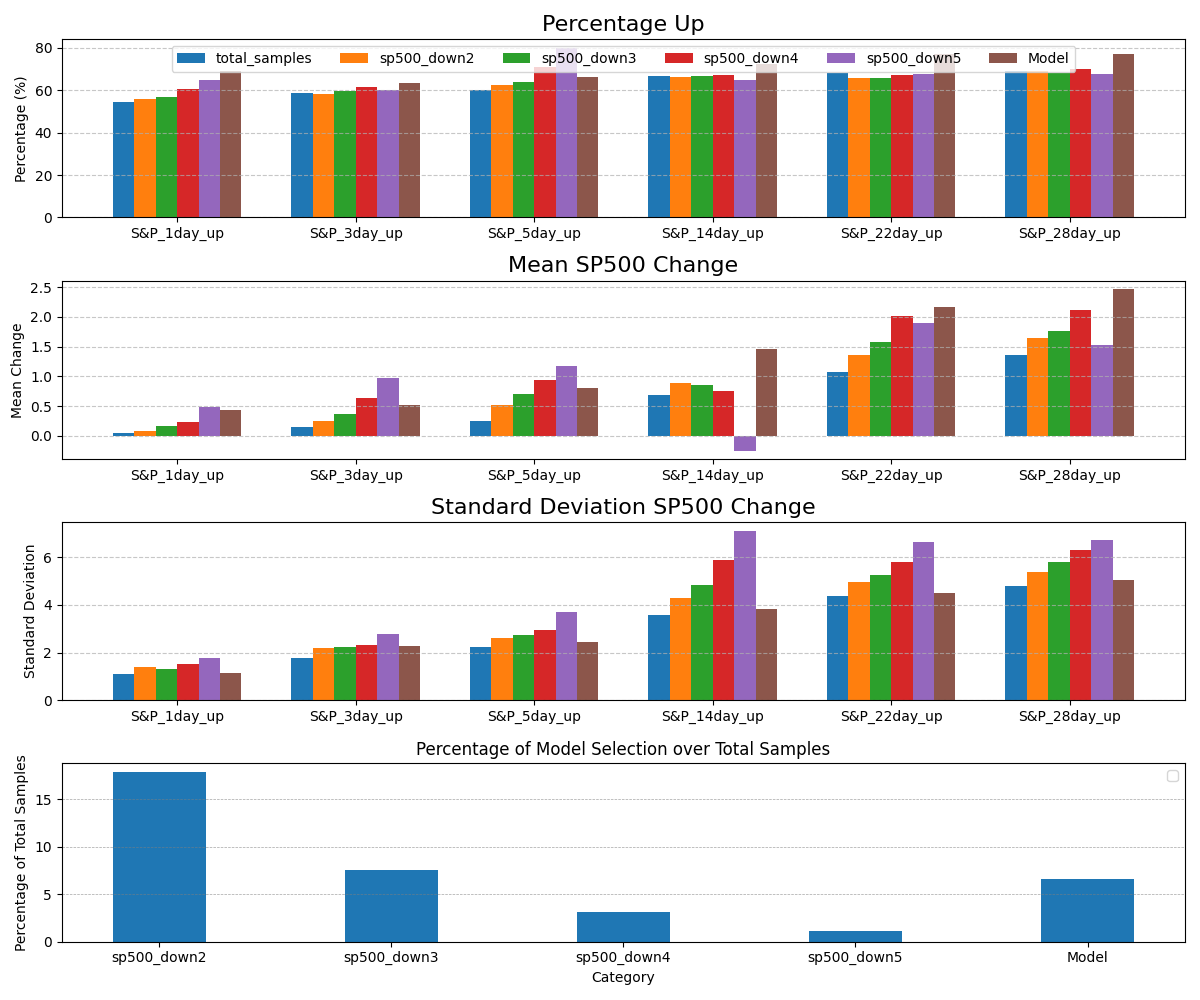

| sp500_down2 | 3447 | 617 | 17.90% | 344 | 55.75% | 0.09 | 1.38 | 358 | 58.02% | 0.25 | 2.19 | 386 | 62.56% | 0.52 | 2.62 | 408 | 66.13% | 0.88 | 4.31 | 406 | 65.80% | 1.36 | 4.96 | 426 | 69.04% | 1.65 | 5.38 |

| sp500_down3 | 3447 | 261 | 7.57% | 148 | 56.70% | 0.16 | 1.33 | 156 | 59.77% | 0.37 | 2.24 | 167 | 63.98% | 0.7 | 2.72 | 174 | 66.67% | 0.85 | 4.85 | 172 | 65.90% | 1.57 | 5.26 | 178 | 68.20% | 1.76 | 5.8 |

| sp500_down4 | 3447 | 106 | 3.08% | 64 | 60.38% | 0.24 | 1.51 | 65 | 61.32% | 0.64 | 2.31 | 75 | 70.75% | 0.93 | 2.93 | 71 | 66.98% | 0.76 | 5.87 | 71 | 66.98% | 2.02 | 5.8 | 74 | 69.81% | 2.11 | 6.31 |

| sp500_down5 | 3447 | 40 | 1.16% | 26 | 65.00% | 0.48 | 1.77 | 24 | 60.00% | 0.98 | 2.77 | 32 | 80.00% | 1.18 | 3.69 | 26 | 65.00% | -0.25 | 7.12 | 27 | 67.50% | 1.89 | 6.66 | 27 | 67.50% | 1.53 | 6.71 |

Key Metrics

1-day performance:

Control: 54.31% of days are up, with a mean return of 0.05%.

Model: 68.86% of selected days are up, with a mean return of 0.43%.

3-day performance:

Control: 58.92% of days are up, with a mean return of 0.15%.

Model: 63.60% of selected days are up, with a mean return of 0.52%.

5-day performance:

Control: 60.34% of days are up, with a mean return of 0.25%.

Model: 66.23% of selected days are up, with a mean return of 0.80%.

14-day performance:

Control: 66.58% of days are up, with a mean return of 0.69%.

Model: 72.37% of selected days are up, with a mean return of 1.46%.

22-day performance:

Control: 68.90% of days are up, with a mean return of 1.08%.

Model: 77.19% of selected days are up, with a mean return of 2.17%.

28-day performance:

Control: 68.90% of days are up, with a mean return of 1.36%.

Model: 77.19% of selected days are up, with a mean return of 2.47%

Summary: The model outperforms the control group consistently across all trading intervals, achieving significantly higher percentages of "up" days and greater average returns.

This demonstrates that the model is effective in identifying favorable entry points compared to random selection.

The standard deviations between the model and the control are similar, indicating comparable variability in performance.

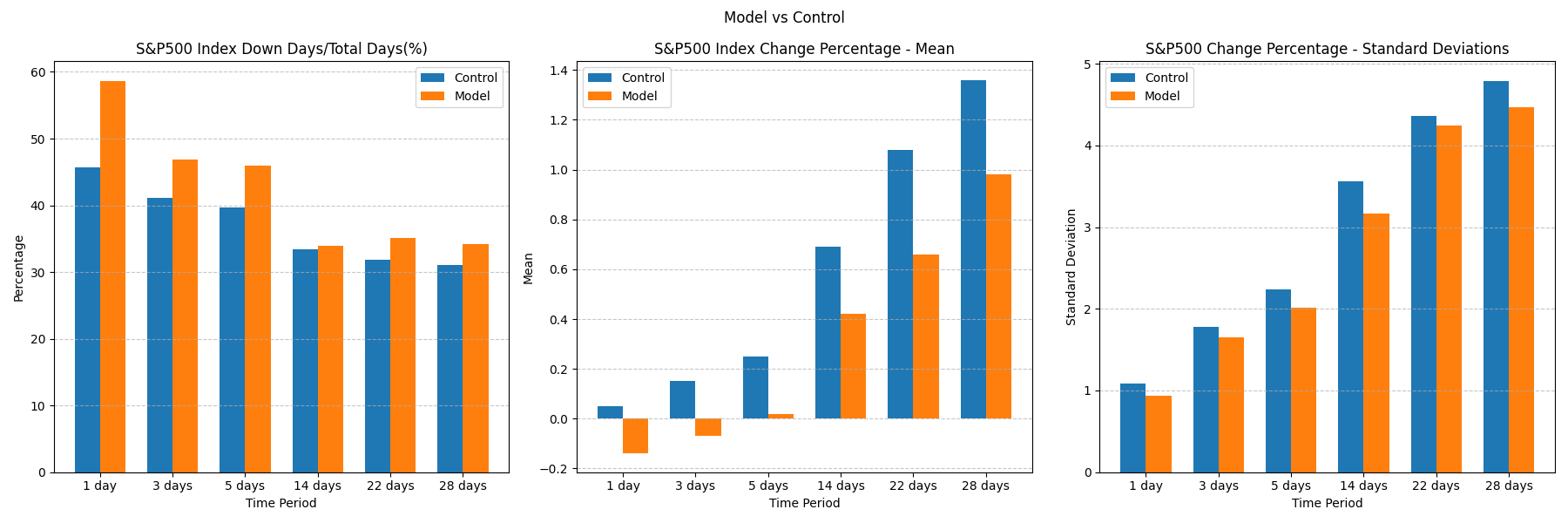

Percentage Up (Top Chart): This chart shows the proportion of SP500 up days over the specified time intervals (1, 3, 5, 14, 22, and 28 days) for different groups: total samples (control), continuous SP500 down days (2, 3, 4, 5 days), and the model's selected days.

The model demonstrates a higher percentage of SP500 up days compared to the control and other scenarios, indicating its superior ability to identify favorable trading days.

Mean SP500 Change (Second Chart): This chart depicts the average SP500 returns over the same time intervals for each group. The model outperforms the control and most other scenarios in terms of mean SP500 return. While SP500 down5 sometimes shows competitive returns, its small sample size limits statistical reliability.

Standard Deviation SP500 Change (Third Chart): This chart compares the variability (standard deviation) of SP500 returns across groups. The model maintains relatively low variability, which suggests consistent performance compared to the other groups, where variability tends to be higher, particularly for SP500 down5.

Percentage of Model Selection Over Total Samples (Bottom Chart): This chart highlights the proportion of trading days selected by each method (model and SP500 continuous down scenarios). The model selects a substantial number of trading days compared to SP500 down5, which, despite its occasional strong performance, suffers from a significantly smaller sample size, reducing its statistical significance. SP500 down2 has the highest selection percentage among the scenarios but does not match the model's overall performance metrics.

Summary: The model excels in selecting trading days with a high percentage of SP500 up days, strong average returns, and low variability.

Although specific scenarios (e.g., SP500 down5) occasionally show competitive results, their small sample size limits their reliability, making the model a more consistent and statistically significant performer.

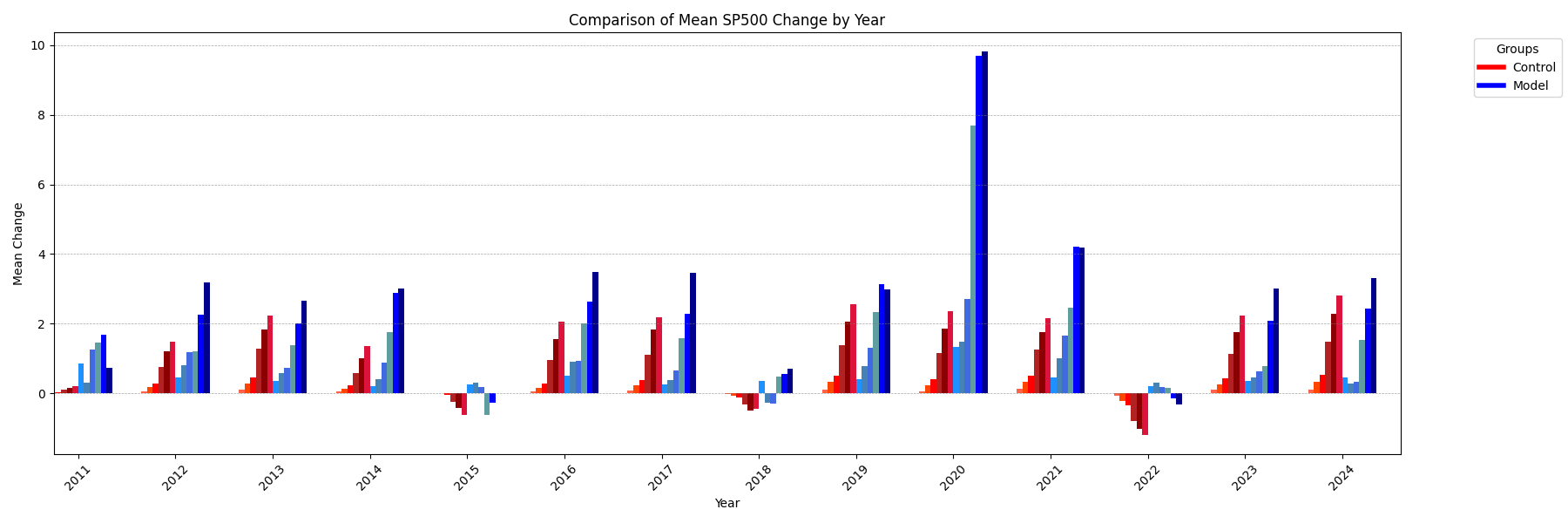

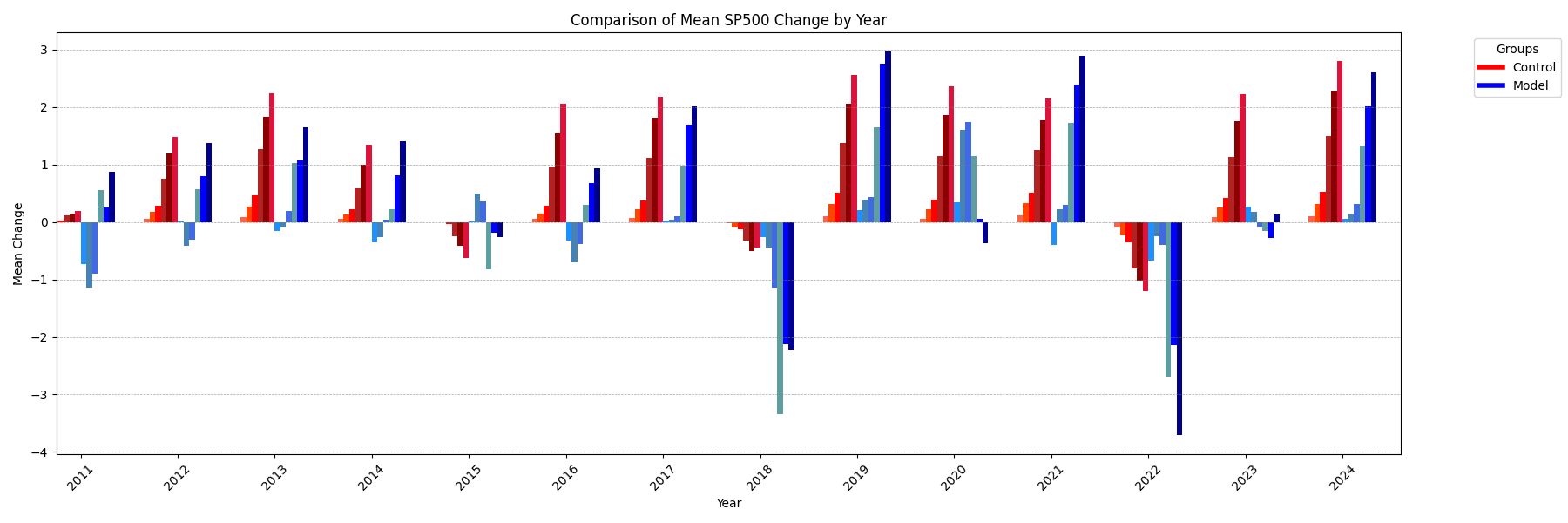

Consistent Outperformance: The model generally shows higher mean SP500 changes compared to the control across most years. This demonstrates the model's consistent ability to identify trading days with better returns than random sampling.

Yearly Variability: In some years (e.g., 2020 and 2021), the model's performance is significantly higher than the control, reflecting strong market opportunities identified by the model. Even in years with smaller returns (e.g., 2016 or 2022), the model still outperformed the control group.

Resilience in Down Years: During years with negative market performance (e.g., 2022), the model shows less severe negative returns compared to the control, suggesting better downside protection.

Summary: The model demonstrates consistent and significant outperformance of the control group over the years, both in up and down markets. This highlights the model's robustness in selecting trading days with superior SP500 returns across varying market conditions.

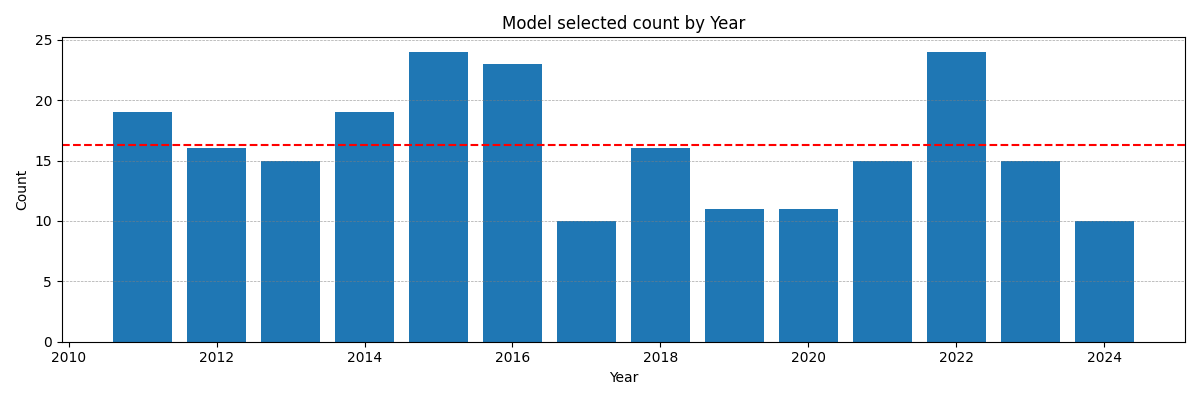

Potential Influence of Market Trends: High counts in years like 2015 and 2022 could correspond to higher market volatility or more pronounced downside trends. Lower counts in years like 2020 and 2024 may align with more stable or upward-trending markets.

Analysis of the Model Focusing on SP500 Down Days

Total Sample Size: 3447 ( started from 2011-01-12 )Model Selected Count: 293 (out of 3,447 trading days, the model selected 293 specific days).

Model Selected Percentage: 8.49% The market performance is evaluated at intervals of 1, 3, 5, 14, 22, and 28 days following the model's selected dates. The model's performance is assessed based on the 293 selected days, while the control group's performance is measured using all available samples. Generally, trading days chosen by the downside-focused model show smaller SP500 gains compared to the control group. However, this performance is inconsistent, as illustrated in Figure 6.

Effectiveness: The model demonstrates superior performance in identifying SP500 down days and capturing negative trends compared to the control group.

Strengths: It performs best over shorter time periods (1-5 days) and retains its edge over longer time periods, albeit with slightly higher variability.

Implication: This supports the conclusion that the model adds value for strategies focused on downside protection, particularly for shorter-term trades or risk mitigation.

General Outperformance in Down Markets: The model shows significant outperformance during bearish years like 2018 and 2022, where the S&P 500 experienced noticeable negative mean changes. This aligns with the model’s focus on identifying negative signals.

The blue bars (model) in these years are notably higher than the red bars (control), indicating that the model was effective in capturing downside risk.

Inconsistent Performance in Bullish Years: During strong market years (e.g., 2013, 2017, 2023), the model struggles to match the performance of the control group. This suggests that the model's design for identifying negative signals might not adapt well to upward market trends.

Overall Model Edge: Across the years, the model generally shows a slight edge over the control group. This is evident from the more frequent occurrence of higher blue bars compared to red bars.

However, the edge seems stronger in bear markets compared to bull markets, emphasizing that this model is more specialized in detecting negative sentiment.

Variability Across Years: The model's performance is not consistent year over year. This could be due to differences in market conditions, volatility, or external factors that may not align with the signals the model is optimized for.

Conclusion: The downside-focused stock model demonstrates clear value in detecting and mitigating risk during bearish periods, showing a distinct advantage over random selection.

However, it faces challenges during bullish years, where its performance becomes inconsistent or lags behind the control group. This could be an area for refinement if the goal is broader applicability across all market conditions.